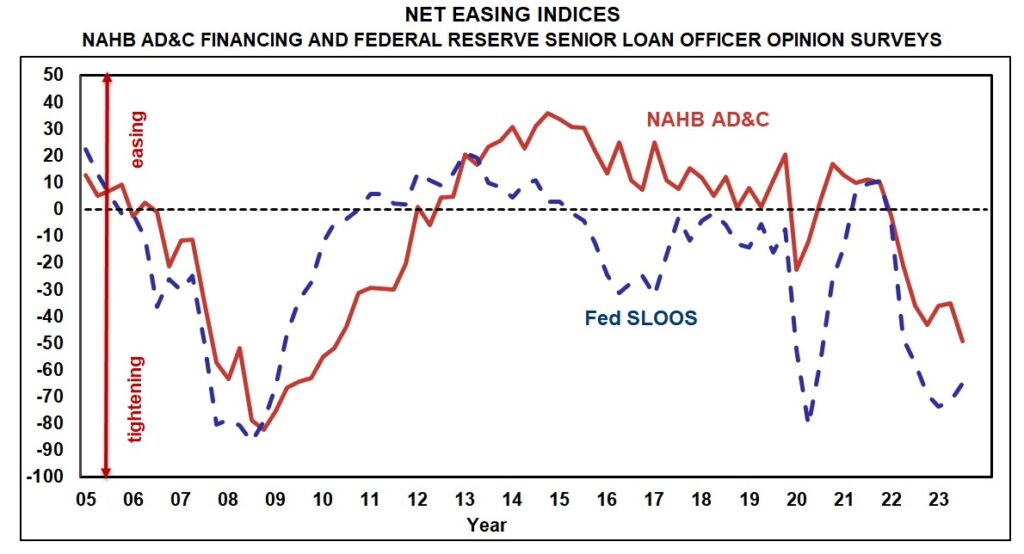

During the third quarter of 2023, availability of loans for residential Land Acquisition, Development & Construction (AD&C) continued to tighten, according to both NAHB’s survey on AD&C Financing and the Federal Reserve’s survey of senior loan officers. Each of the surveys produces a net easing index that is positive when credit is easing and negative when credit is tightening.

In the third quarter, both the NAHB and Fed indices were negative, indicating that builders and lenders were once again in agreement that credit was, on net, tightening. The NAHB index posted a reading of -49.3—considerably below the -35.3 posted in the second quarter and the most widespread reporting of tightening by builders since the 2010 trough of the Great Recession.

Lenders’ reporting of tightening was even more widespread in the third quarter, as the Fed’s net easing index posted a reading of -64.9 (compared to -71.7 in the second quarter). Historically, both the Fed and NAHB indices shifted from indicating net easing to net tightening at the start of 2022 and have now been solidly in negative territory for the last seven quarters. Additional results from the Fed survey were reported in last Friday’s post.

According to the NAHB survey, the most common ways in which lenders tightened during the third quarter were by increasing the interest rate on the loans (cited by 80% of the builders and developers who reported tighter credit conditions), reducing amount they are willing to lend (57%) and lowering the allowable Loan-to-Value or Loan-to-Cost ratio (52%).

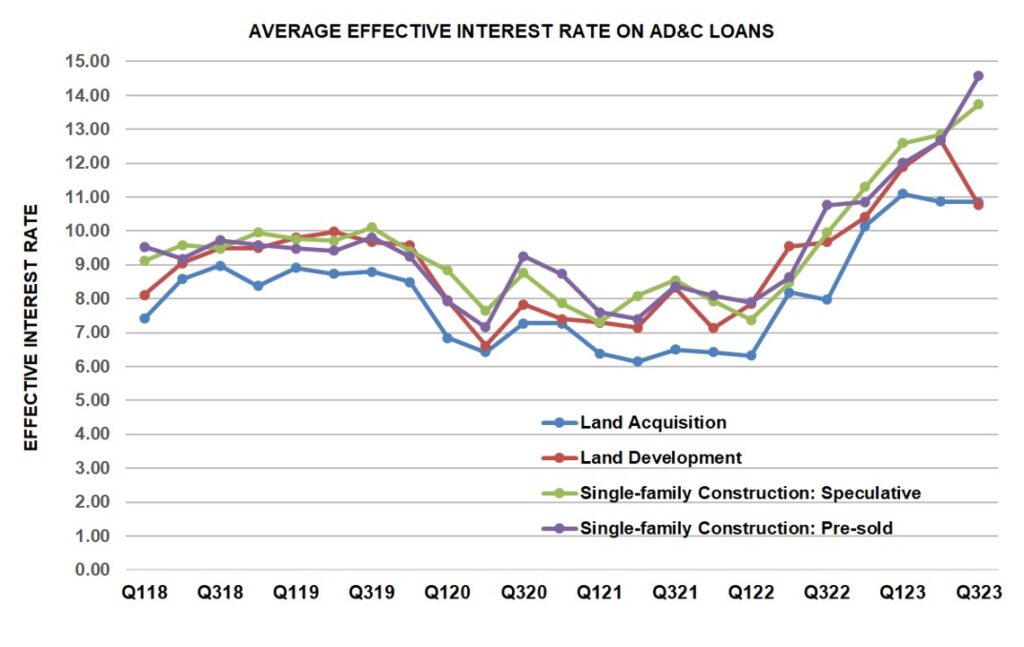

What happened to the cost of credit during the third quarter depended on if you were a builder or developer. On loans specifically for single-family construction, the average contract interest rate increased—from 8.37% to 8.66% if the construction was speculative, and from 8.18% to 8.37% if it was pre-sold. In contrast, the average contract rate declined on loans for land acquisition (from 8.62% to 8.31%) and land development (from 8.70% to 7.78%).

Although the average initial points also declined (from 0.81% to 0.58%) on loans for land development, it increased on the other three categories of loans tracked in the NAHB AD&C survey: from 0.52% to 0.86% on loans for land acquisition, from 0.71% to 0.93% on loans for speculative single-family construction, and from 0.44% to 0.86% on loans for pre-sold single-family construction.

The above changes caused the average effective interest rate (rate of return to the lender over the assumed life of the loan, taking both the contract interest rate and initial points into account) paid by developers to decline. The decline was very small (only two basis points from 10.87% to 10.85%) on loans limited to land acquisition, but more substantial (nearly two full percentage points from 12.67% to 10.76%) on the more general category of loans for land development. Even after these reductions, however, the effective rate on A&D loans remained higher than at any time between 2018 (when the cost of credit questions were added to the survey) and 2022.

The effective rate paid by single-family builders on construction loans, meanwhile, continued to climb much as it had over the previous five quarters: from 12.85% to 13.74% on loans for speculative construction, and from 12.67% to 14.57% on loans for pre-sold construction.

Discover more from Eye On Housing

Subscribe to get the latest posts to your email.