Residential construction loan volume reached a post-Great Recession high during the second quarter of 2022, as home building activity and new home sales slowed. Outstanding builder loan balances are rising as development debt is being held longer as new homes remain in inventory longer. Loan balances will decline in coming quarters as the development loan market becomes more costly and tighter given higher interest rates. This is a reminder that tighter monetary policy affects housing demand but housing supply as well.

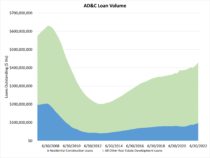

The volume of 1-4 unit residential construction loans made by FDIC-insured institutions increased 5% during the second quarter. The volume of loans increased by $4.7 billion on a quarterly basis. This loan volume expansion places the total stock of home building construction loans at $97.1 billion, a post-Great Recession high.

On a year-over-year basis, the stock of residential construction loans is up 18%. Since the first quarter of 2013, the stock of outstanding home building construction loans has grown by 138%, an increase of more than $56 billion.

It is worth noting the FDIC data represent only the stock of loans, not changes in the underlying flows, so it is an imperfect data source. Lending remains much reduced from years past. The current amount of existing residential AD&C loans now stands 52% lower than the peak level of residential construction lending of $204 billion reached during the first quarter of 2008. Alternative sources of financing, including equity partners, have supplemented this capital market in recent years.

The FDIC data reveal that the total decline from peak lending for home building construction loans continues to exceed that of other AD&C loans (nonresidential, land development, and multifamily). Such forms of AD&C lending are off a smaller 24% from peak lending. For the second quarter, these loans posted a 3.7% increase.

Discover more from Eye On Housing

Subscribe to get the latest posts to your email.